In 2022 and 2023 craft beer saw it first significant decline in volume in decades. Overall beer is down 4% in general and craft is down 7% as a category (from the Brewers Association). What is causing this category – for so long the darling of the alcoholic beverage world to wither now? There are many opinions, many facts and figures, but no one is 100% certain.

Craft Beer is not dead in any manner – in fact new breweries opening continue to outpace breweries closing – a net gain of over 200 new breweries opened last year putting the total numbers of breweries at almost 9,500 in the US.

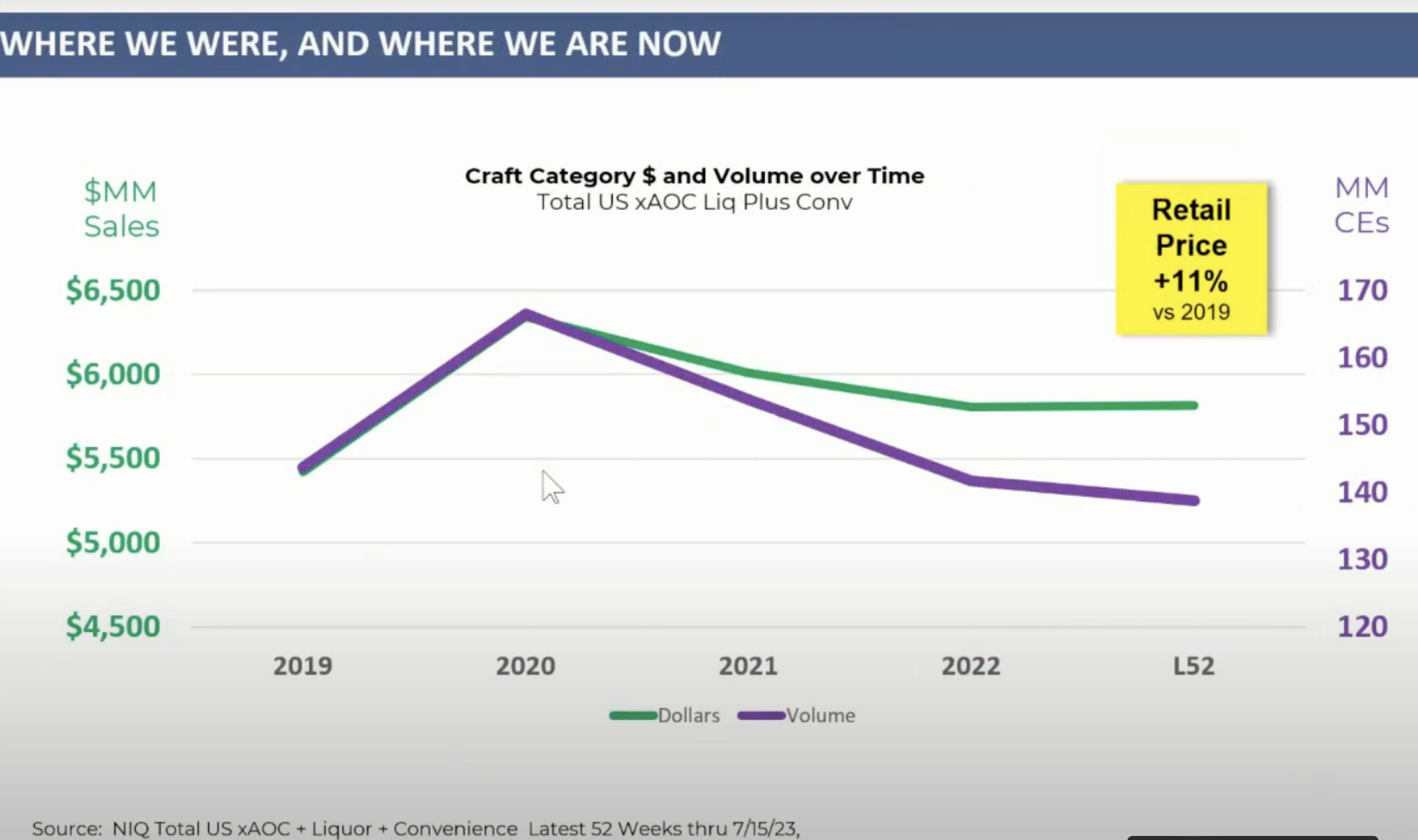

Prices are up and so dollar volume has not declined so much. (Though recent data suggests that inflationary forces are starting to show cracks in consumer spending patterns on craft as well).

That said, the numbers for the existing breweries for most of the traditional craft brands you know are down, and significantly. Sierra Nevada, Dogfish Head, Sam Adams, Firestone Walker are all down. Lagunitas is off nearly 12% in past year alone. But where is craft still growing? Mostly in two places – the smallest local tap rooms and the largest regional craft breweries. New Belgium (owned by Japan’s Kirin) is up 25% and Goose Island (owned by Belgium’s AB Inbev) is up 26%. The big guys are rolling, able to absorb economic headwinds with scale, efficiency and distribution. The littlest guys – can still be profitable with very small overhead and direct sales to consumers through local tap rooms. Those breweries in the middle are generally just trying to hang in there while others continue to lose share.

9.5% Juicy IPA is the way

So, what is going on? Industry discussions and research suggest a number of factors – some cultural, some economic and others demographic that seem to lean away from craft beer. In no particular order, what follows is a list of those factors most commonly mentioned:

Demographics – Baby boomers were the craft beer champions. They are aging out of traditional beer drinking age and their position of being the majority of the population. Millennials also supported craft but are being displaced by Gen Z who are not interested in “yuppy beer” or even alcohol in general in comparison. People of color and woman have increased significantly in drinking age population – now more women are of drinking age below 25 than men. These two groups traditionally don’t drink that much craft beer.

Consumer Preferences – Now more people of drinking age want choices and alternatives. They are as much interested in “FMB’s” (Fermented Malt Beverages like Hard Tea and Lemonade) and hard seltzer as beer. They also like the “ready to drink” cocktails in cans – and want to drink any of these at any time or occasion. Due to health concerns NA (non alcoholic) beer continues to grow at a breakneck pace -such that Athletic Brewing’s NA beers are now considered a top 15 craft brand. Craft beer consumers are also showing less interest in “beer flavored beer” instead trying sweeter brews like “pastry stouts” and “milkshake IPA’s”. This enables cross over to other non beer flavored alcoholic beverages to becomes more blurred.

Many choices at the beer shelf – and they are not all beer

Declining Investor Interest in Funding Breweries – Long gone are the days that people bought into breweries for the fun and panache of being a brewery owner, with little expectation of economic return. That patience has seemingly dried up and now interest in investing in breweries has similarly evaporated. The largest macro-breweries who jumped on the craft bandwagon in the 2000’s are now divesting their craft acquisitions as their profitability dwindles.

Competition in the Space is Fierce – The proliferation of craft beers in the past few years made it hard for consumers and distributors to keep up. Shelf space and tap handles are in turmoil and then there’s the growth of the FMB’s, N/A’s and seltzers. The consumer preference for “something new” has created a glut of choices, forcing breweries to adopt new strategies and niche’s to stand out from the noise. Brand loyalty is a disappearing concept, and craft distributors are looking to reduce brands to make distribution more efficient.

Economic Headwinds – Costs of brewing supplies and equipment continue to go up. Supply chain issues – for everything from cans to C02 – while improving – still exist. Cost of funding loans for expansion and new equipment is significantly higher than recent past. The larger brewing companies are better equipped to withstand these shifts in expenses than smaller players – which is more critical in an industry with so many small players.

NA Beer is the fastest growing “craft” category

COVID – While during the height of the pandemic packaged beer sales soared, yet post pandemic volume – particularly on premise draft – has never fully recovered. During the lockdown and after, people changed their lifestyle habits. They didn’t go back to the bars they used to frequent. They now prefer to buy their beer out and bring it home. Currently the largest single channel of growth in all types of alcohol sales are from convenience stores. And the most popular type of package to buy today is the single 19 oz can or the 12 pack. Six packs are fading away, and as mentioned draft beer sales – except in small craft beer taprooms – are way down. This is the “new normal”.

Maturation of the Industry. In and around the 1990’s craft beer was more than an industry, it was a “movement”. It was a tribe of renegades crafting their own exotic products in competition with huge, faceless, money-grubbing corporate breweries. Home brewers became commercial brewers, people poured their life savings into half baked concepts and learned as they went along. Many failed while others like Sierra Nevada, Dog Fish and New Belgium became industry leaders.

There was an ethos and purpose that went beyond financial gain and commercial production in craft. That spirit is mostly gone, replaced with business plans, cautious investors and brewing efficiency. Innovation is shrinking while growth declines. It’s hard to be a renegade when jobs and investors are big time considerations. Many breweries are selling off excess capacity and “right sizing” for efficiency. Most of today’s craft drinkers don’t know (or care) if their beer is made locally, by a huge conglomerate or a foreign based corporation. Craft is a business.

So, will craft beer survive? I think it will, as for every Anchor Steam that closes and brewery that downsizes, new smaller breweries spring up. Many brewery owners are classic American entrepreneurs – and we know what they can do. Sure there are many changes, issues and challenges for craft brewers to confront, but America has been brewing for over 150 years and it still survives. It probably just won’t be your “father’s craft beer” you’ll be drinking, it will be something new again, and it will be good to drink.

Craft Beer will endure because it’s good!